Contact Us

7410 South Creek Road Ste 203, Sandy UT 84093

7410 South Creek Road Ste 203, Sandy UT 84093

801-748-3533

7410 South Creek Road Ste 203, Sandy UT 84093

801-748-3533

801-748-3533

7410 South Creek Road Ste 203, Sandy UT 84093

801-748-3533

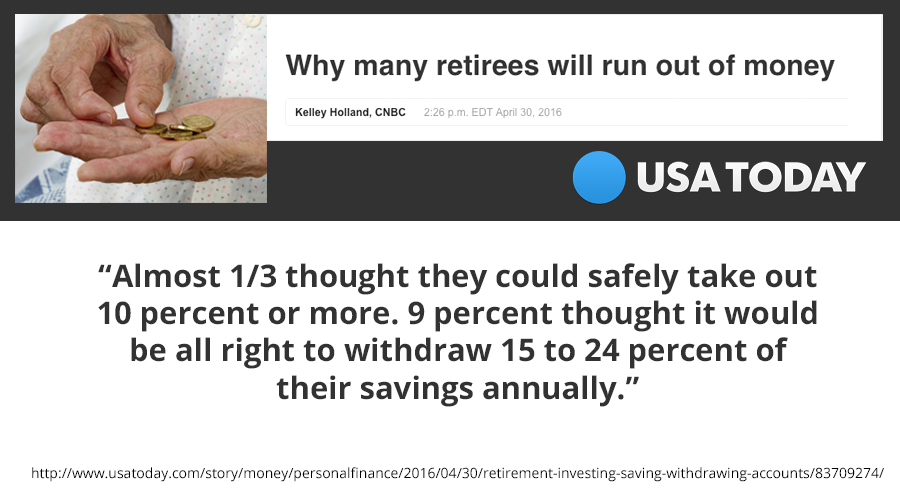

http://www.usatoday.com/story/money/personalfinance/2014/11/08/cnbc-four-percent-withdrawal-retirement-rule/18509395/

http://www.cnbc.com/2014/11/03/the-4-retirement-rule-is-broken-and-heres-why.html

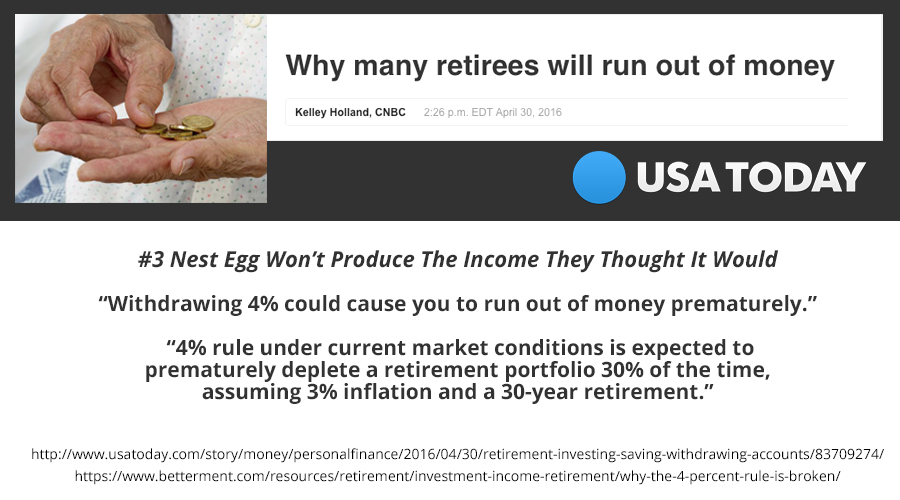

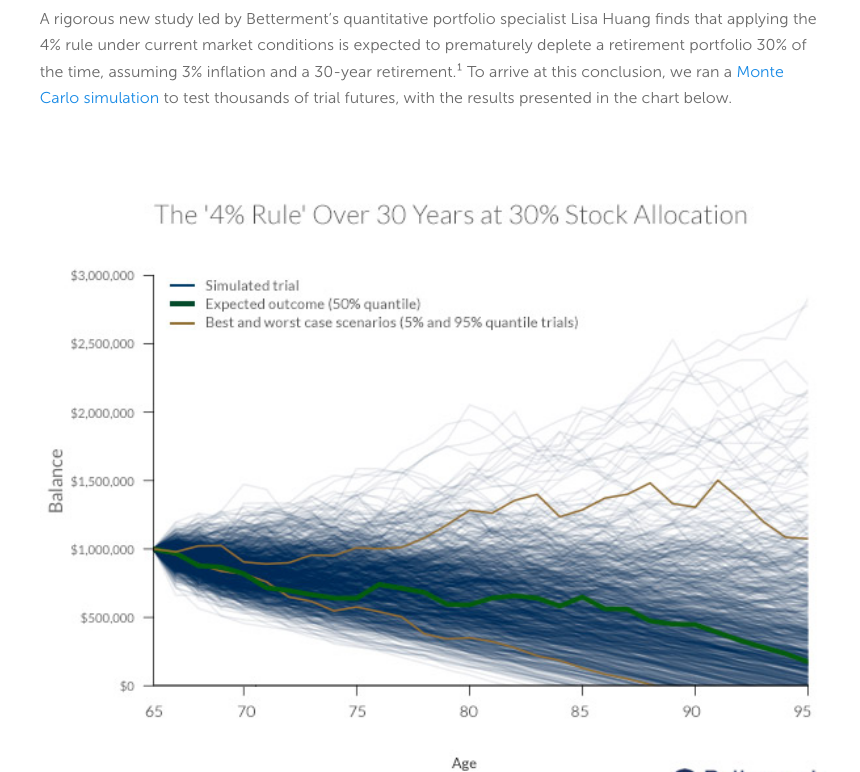

4% rule under current market conditions is expected to prematurely deplete a retirement portfolio 30% of the time, assuming 3% inflation and a 30-year retirement.

In the 1990's when the 'rule' was created, the yield on a three-month Treasury bill was 6%.

That's no longer the case—today a three-month Treasury is .04% and a 5-year is around 1.67%.

https://www.betterment.com/resources/retirement/investment-income-retirement/why-the-4-percent-rule-is-broken/